Welcome to Interport Global Logistics Newsletter

June 2025, Volume # 011

The Shift Is On: Why the World’s Big Brands Are Betting on Made-in-India

Ask any Gen Z teen about Shein, and they’ll likely have a cart full of wishlisted outfits ready to go. The fast-fashion powerhouse has become a global obsession — and now, it’s turning to India for manufacturing. But this isn’t just about trendy tops or bargain dresses. It’s part of a much broader story unfolding quietly but steadily: India is having its manufacturing moment.

The reason? One word: strategy.

As global tensions simmer — especially between the U.S. and China — businesses are rethinking their supply chains. From fashion to phones, semiconductors to aerospace, companies are scouting for new, reliable locations to build and export. And increasingly, India is making the shortlist.

Let’s start with Apple. Manufacturing partner Foxconn has pledged $1.5 billion to expand its iPhone plant in Tamil Nadu. Just a few years ago, only a tiny fraction of iPhones came out of India. Today, that figure is around 18%, and it’s expected to grow to 25% by 2027. In 2024-25 alone, smartphone exports from India hit $24.14 billion — a 55% surge over the previous year.

Google is making similar moves. It has announced plans to assemble Pixel smartphones in India, partnering with Dixon Technologies. The goal? To tap into one of the world’s fastest-growing smartphone markets and double hardware revenue in the region.

And it’s not just tech.

Vietnam’s electric vehicle maker VinFast is building a $2 billion plant — again in Tamil Nadu — aiming to make India a key export base for its cars. Aerospace heavyweights like Airbus and Pratt & Whitney are also sourcing more components from Indian suppliers. According to India’s Ministry of Commerce, aerospace exports grew by 38% year-on-year in 2023–24.

Clearly, this shift goes far beyond Shein. What we’re witnessing is a strategic realignment — a move by global businesses to spread their risks and reduce overdependence on any single geography.

The backdrop? A tense and uncertain global environment. The U.S.-China trade relationship remains frosty, with tariffs and tech restrictions stretching across multiple presidential terms. Security concerns, data regulations, and political unpredictability only add fuel to the fire.

To manage these risks, companies are adopting what many now call a “China + 1” approach — and India is becoming the +1 of choice.

Why India? Several reasons. A large, youthful workforce. A stable democracy. And proactive government support, especially through initiatives like the Production-Linked Incentive (PLI) scheme launched in 2020. This scheme spans key sectors including electronics, pharmaceuticals, textiles, and solar modules — attracting over $33 billion in committed investments so far.

But let’s not paint an overly rosy picture.

India still faces serious challenges. Labor concerns have been flagged in sectors like cotton farming, and logistical bottlenecks remain in certain regions. The World Bank’s 2023 Logistics Performance Index ranks India 38th — a step forward, yes, but still behind peers like Malaysia and Thailand.

Infrastructure, bureaucracy, and execution risks persist. These are not deal-breakers — but they’re not footnotes either.

Despite this, the global mood is shifting. It’s no longer just about finding the cheapest supply chain — it’s about building one that’s resilient. The pandemic, port disruptions, and geopolitical tremors have forced companies to prioritize flexibility and risk mitigation.

In that equation, India offers a compelling alternative. Not a replacement for China, but a partner in building a more balanced global manufacturing map.

Nomura’s 2023 report reflected this shift. While India gained share in sectors like electronics and machinery, countries like Vietnam, Mexico, and Bangladesh also saw growth. But in a 2025 follow-up, Nomura emphasized that India stands to be one of the biggest winners in the next phase of global supply chain diversification.

So, this isn’t a zero-sum game where one nation wins and another loses. It’s a reshuffling of global bets — where companies weigh cost, stability, incentives, and political alignment.

For investors, India’s rise brings both opportunity and caution. The upside? A booming domestic market, soaring exports, and a strong inflow of foreign capital. The risks? Structural challenges and a reform curve that’s still unfolding.

In the end, India’s manufacturing story isn’t just about what’s happening on the factory floor. It’s about how the global business mindset is changing — cautiously, strategically, and for the long haul.

And that’s why Shein’s story is more than just fast fashion.

It’s a symbol of something much bigger.

World Bank Lowers Global Growth Forecast Amid Rising Trade Tensions

The World Bank has significantly downgraded its global growth outlook for 2025, citing escalating trade tensions and persistent policy uncertainty, particularly following the imposition of broad-based tariffs by the United States. In its latest Global Economic Prospects report released Tuesday, the Bank revised its global GDP growth projection down to 2.3%, from the 2.7% forecast made in January. This downgrade marks one of the steepest adjustments in recent years and underscores growing concerns among global economic institutions.

Nearly 70% of the world’s economies, including the United States, China, and key European nations, are affected by the downward revision. Six major emerging market regions also saw their forecasts cut, continuing a trend of widespread economic recalibration. “This would represent the weakest economic performance in 17 years outside of full-scale global recessions,” noted Indermit Gill, Chief Economist of the World Bank Group.

Gill attributed the weakening outlook to the combination of high policy uncertainty and a noticeable fragmentation in global trade relationships. He warned that without urgent corrective action, there could be significant and lasting damage to global living standards. According to the Bank, global GDP growth is expected to average just 2.5% throughout the 2020s, making it the slowest growth rate for any decade since the 1960s.

Tariff Turbulence

The downward revision comes in the wake of new U.S. tariffs introduced in April, which imposed a 10% duty on imports from most major trading partners. In addition, tariffs on steel and aluminium imports were raised, causing disruptions across global supply chains. Although the U.S. administration has suspended some of these increases until July, the uncertainty surrounding trade policy continues to unsettle markets.

The unpredictability of U.S. trade actions has raised the country’s effective tariff rate from under 3% to levels not seen in nearly a century. Retaliatory measures from China and other major economies have further complicated the landscape, despite a temporary easing of tensions between the U.S. and China.

While advanced economies are seeing sharper proportional growth downgrades, developing countries are also under strain. Many of these nations depend heavily on commodities, and with prices expected to stay low through 2025 and 2026, the economic pressures could deepen. Gill highlighted that around 60% of emerging markets, particularly commodity exporters, now face the double burden of declining prices and heightened market volatility.

Lagging Recovery in Developing Nations

By 2027, per capita GDP in high-income economies is projected to recover to pre-pandemic expectations. However, developing countries—excluding China—may still find themselves 6% below those earlier projections. For some, Gill warned, it could take up to two decades to fully regain lost economic ground.

In addition to slower growth, inflation is now expected to remain elevated, adding another layer of complexity for policymakers. Gill emphasized the need for governments to take decisive action to contain inflation and restore trade stability.

He urged leading economies, particularly the G20, to work towards reducing tariff differentials and removing non-tariff barriers across the board—not just with the U.S., but with all global partners. He also recommended that developing countries move beyond selective trade agreements and aim for broader regulatory harmonization to support long-term growth.

The World Bank’s warnings echo similar recent downgrades from the OECD and the IMF, both of which have cited U.S. tariff actions as a key driver behind weakening global economic forecasts.

Cloudy Waters Ahead: Container Shipping Faces Pressure from Oversupply and Trade Policies

Container shipping companies are bracing for a significant decline in profits in 2025, following a relatively strong 2024 that saw elevated freight rates due to disruptions in the Red Sea. The landscape this year, however, appears far less favourable.

According to Fitch Ratings, global container volumes are expected to remain flat or dip slightly compared to last year, impacted in part by newly imposed U.S. tariffs. This is a shift from earlier forecasts of approximately 3% growth. Meanwhile, global fleet capacity is projected to grow by around 6%, creating a clear mismatch between supply and demand.

Freight rates, which spiked in mid-2024, are already on a downward trajectory. While short-term demand shifts—such as advance shipments ahead of tariff hikes or temporary port congestion—might offer brief support to rates, the overall trend points to continued softening. One key risk is the potential normalization of Suez Canal operations, which could increase global shipping capacity by over 10%, adding further downward pressure.

Complicating the outlook further is the U.S. Trade Representative’s proposed port fee policy, which could introduce significant costs for container shippers—particularly those operating Chinese-built or Chinese-owned vessels. If enacted, non-Chinese companies using Chinese-built ships may face fees of $120 per container starting October 14, 2025, with higher charges anticipated by 2028. Chinese-owned vessels will face even steeper levies. Fitch expects shipping lines to adapt their networks to cushion the impact, though outcomes will vary by operator.

In dry bulk, volume growth remains limited, with Chinese demand continuing to dominate the sector.

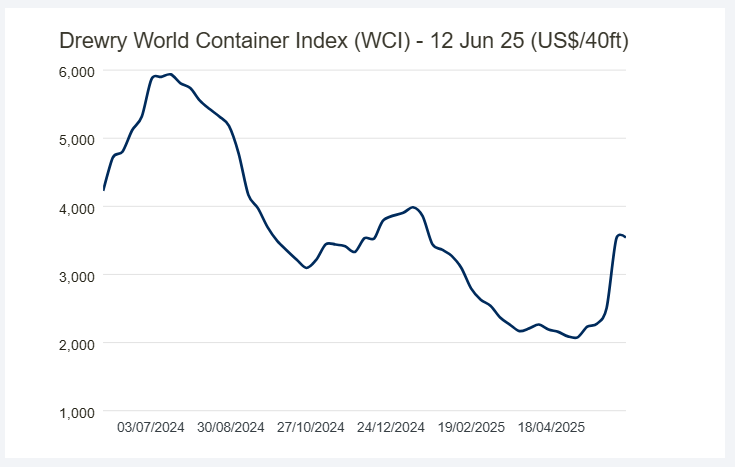

Despite broader challenges, freight rates have recently surged on transpacific routes. Drewry’s World Container Index (WCI) rose 59% over the past four weeks, buoyed by the temporary lifting of import tariffs by President Trump. Spot rates from Shanghai to New York climbed to $7,285 per 40-foot container—up 67% in four weeks—while rates to Los Angeles jumped 89% in the same period.

However, these gains may prove fleeting. Drewry warns that the supply-demand balance is likely to weaken again in the second half of 2025, pushing spot rates back down. The timing and extent of these shifts will hinge on evolving trade policies and how the industry adapts to looming regulatory and capacity challenges.

Dollar Hits Three-Year Low as FTSE 100 Surges to Record High Amid Global Uncertainty

The US dollar slid to a three-year low on Thursday, while London’s FTSE 100 index closed at a record high, reflecting mounting global investor unease over US trade policy and signs of economic softening.

Currency markets saw the dollar decline sharply, with the euro and yen both gaining roughly 1% against it. The greenback has now lost close to 10% of its value against a basket of global currencies since the beginning of the year. Analysts attributed the fall to a combination of subdued US economic indicators and fresh trade tensions sparked by President Donald Trump’s renewed threats of country-specific tariffs.

Meanwhile, the FTSE 100 reached a historic peak of 8,884 points, surpassing its previous record set in March. The rally was driven by a shift in investor sentiment, as market participants sought alternatives to US equities amid growing uncertainty around the American economic outlook.

President Trump stoked volatility on Wednesday by reaffirming plans to impose targeted tariffs in the coming weeks. “We’re going to be sending letters out in about a week and a half, two weeks, to countries, telling them what the deal is,” he stated during a Washington event.

Adding to investor jitters were expectations that the US Federal Reserve may begin cutting interest rates sooner than previously anticipated. Recent data showed both consumer and producer inflation weakening, while job market figures also disappointed. The four-week average of jobless claims rose to 240,250 in May — the highest level since August 2023.

Kit Juckes, chief FX strategist at Société Générale, noted “clear and persistent dollar selling” across markets. Neil Wilson of Saxo Markets pointed to a broader trend: “Investors are diversifying geographically. For the first time in years, people are questioning the ‘There Is No Alternative to America’ narrative.”

US-India trade tensions also grabbed headlines, with disagreements around steel and pharmaceutical imports potentially leading to retaliatory tariffs from New Delhi. Bloomberg reported that Indian officials objected to US demands, including the acceptance of genetically modified crops and relaxed price caps on medical devices.

On a brighter note for the UK, Donald Trump signaled support for activating a bilateral trade agreement recently signed with Prime Minister Keir Starmer. UK Trade Secretary Jonathan Reynolds said this could result in reduced tariffs on British car exports, while also opening UK markets further to American beef and ethanol.

However, the British pound’s rise toward $1.36 was tempered by concerns over domestic economic performance. A 0.3% contraction in April raised expectations that the Bank of England could lower interest rates sooner than expected, possibly as early as August.

According to Aviva Investors' economist Vasileios Gkionakis, the dollar’s extended decline reflects investor doubts about the US economy’s future performance under current policies and rising debt levels, which are weighing on confidence.

The content shared herein is provided ‘as is’ and it is for the informational purpose only. No legal or financial advice or professional consultation is intended or implied. Interport Global Logistics or the author (s) shall not be held liable for any direct, indirect, incidental, special or consequential damages arising from the use or reliance on any of the information shared in. For more information contact Interport Global Logistics.